The State of UK Search at the Start of 2025

January 2025 felt like the calm before a very significant storm.

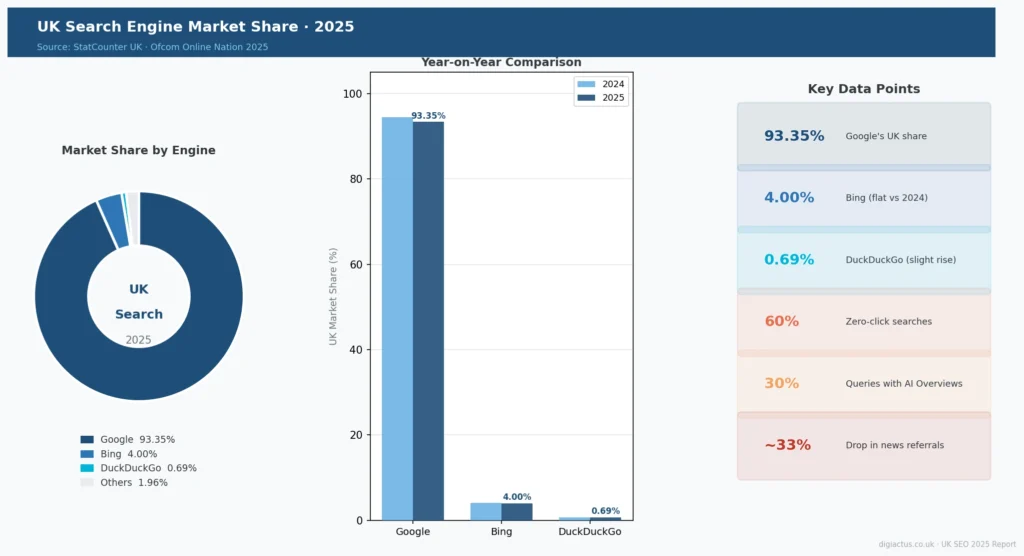

Google still dominated UK search with around 93–94% market share. Bing sat at about 4%. DuckDuckGo held roughly 0.7%. Those numbers looked stable. But underneath them, something important was already shifting.

ChatGPT had been growing rapidly throughout late 2024. UK users were increasingly turning to AI tools for answers they used to type into Google. And on the regulatory side, something historic was about to happen.

On 1 January 2025, the Digital Markets Competition and Consumers Act 2024 (DMCCA) came into force. For the first time, UK regulators had real legal teeth to tackle Big Tech dominance in digital markets. Just two weeks later, on 14 January, the Competition and Markets Authority (CMA) launched a formal investigation into Google’s search and advertising markets under this new law.

The SEO industry sensed change was coming. Most agencies were still operating on traditional keyword-and-backlinks strategies, but the more forward-thinking ones were already asking: how do we optimise for AI answers, not just search rankings?

As it turned out, they were right to ask.

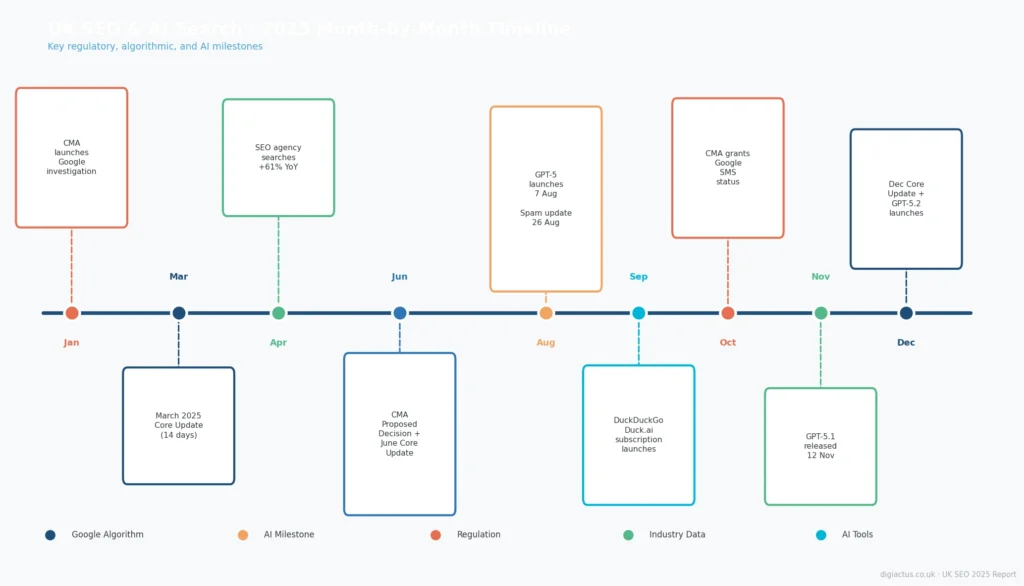

Month-by-Month: 2025 UK SEO Timeline

The key events in UK SEO during 2025 were: the CMA investigating Google (January), the March and June core algorithm updates, GPT-5 launching in August, Google’s August spam update, the CMA designating Google with Strategic Market Status in October, GPT-5.1 arriving in November, and the December core update closing the year.

Here is a verified, month-by-month breakdown of what happened.

January 2025 — Regulation Begins

- 1 January: The DMCCA comes into force. The CMA gains new powers over Big Tech.

- 14 January: The CMA formally investigates Google’s search and advertising markets. This is the first investigation under the new regime.

- Industry mood: cautiously optimistic. Most UK marketers were focused on recovering from Google’s December 2024 core update, which had completed on 18 December.

February 2025 — Relative Calm

No major algorithm updates. However, Google signals that it plans more frequent core updates in 2025. ChatGPT usage in the UK continues climbing steadily. UK businesses begin experimenting more seriously with AI content tools.

March 2025 — First Core Update of the Year

- 13 March: Google releases its March 2025 Core Update. It completes on 27 March — a 14-day rollout.

- The update was described by Search Engine Land as “a typical core update” but less widespread than some 2024 updates. Sites that were affected saw significant ranking swings.

- Forum content and user-generated material, which had been boosted since 2023, began to see corrections.

- Google repeated its standard advice: create helpful, people-first content.

April 2025 — Agency Demand Explodes

- 4 April: Koozai publishes its UK Search Trends Report. The headline findings are striking. Searches for “SEO agency” are up 61% year-on-year. Searches for “PPC agency” are up 115%.

- This is not just curiosity — it reflects real buying intent. Businesses are scrambling for expert help as the search landscape grows more complex.

May 2025 — AI Overviews Expand Quietly

Google continues rolling out AI Overviews in the UK. More query types trigger AI-generated answer summaries at the top of results. Click-through rates for organic results start declining. The CMA’s consultation on Google’s proposed Strategic Market Status designation picks up pace.

June 2025 — Second Core Update and a Regulatory Milestone

- 24 June: The CMA publishes its Proposed Decision, provisionally designating Google with Strategic Market Status in search.

- 30 June: Google releases the June 2025 Core Update. It completes on 17 July — a rollout of 16 days and 18 hours. This update is notably more volatile than the March update. YMYL sectors (health, finance, news) feel the greatest impact. Some sites penalised by Google’s 2023 Helpful Content Update begin to see partial recoveries.

July 2025 — Second Wave Volatility

The June update continues causing SERP fluctuations through to 14 July. The CMA publishes its Search Roadmap in mid-July, outlining possible remedies: choice screens, data portability, fair ranking requirements, and publisher attribution rules.

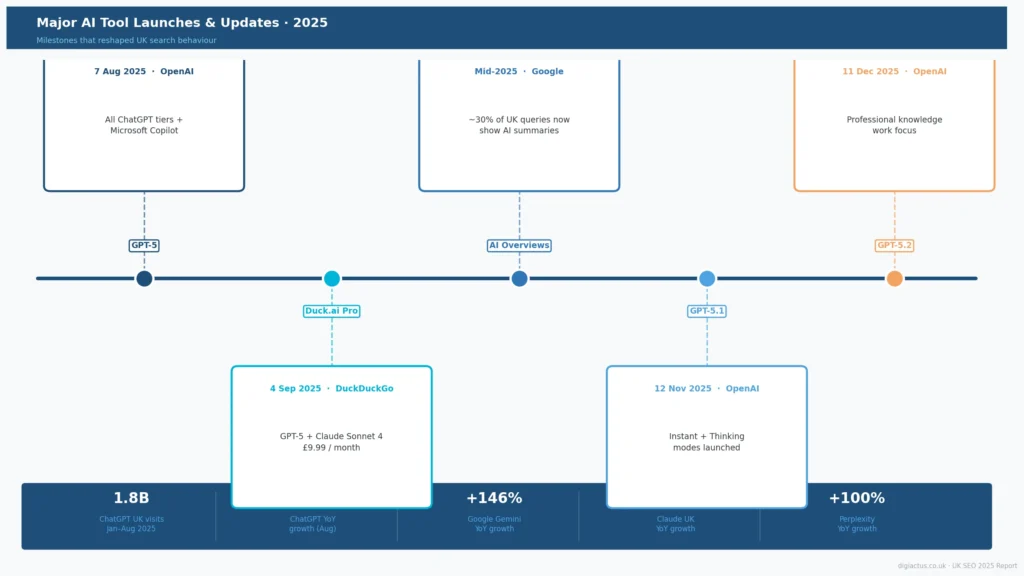

August 2025 — GPT-5 Changes the Game

- 7 August: OpenAI launches GPT-5 publicly, available to all ChatGPT users and via API. Microsoft integrates it into Copilot. GPT-5 features adaptive reasoning modes, improved multimodal capabilities, and significantly fewer errors. Its launch is widely covered as a defining moment for AI search.

- 26 August: Google releases its August 2025 Spam Update, focused on manipulative link schemes and low-quality backlink profiles.

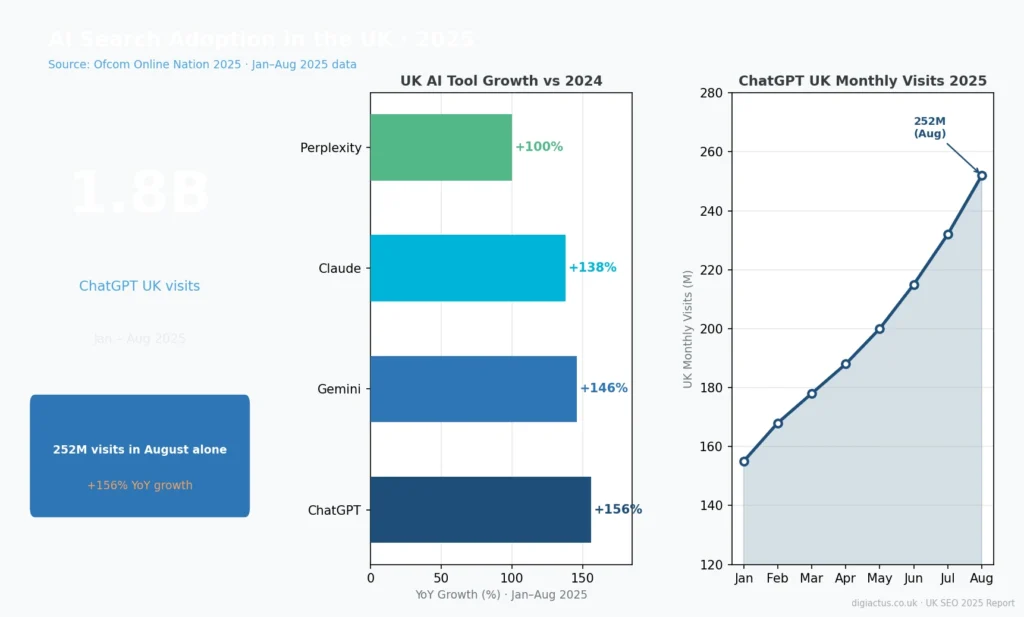

- Ofcom data collected around this period (published in December) later reveals: ChatGPT received 252 million UK visits in August 2025 alone — a 156% year-on-year increase versus August 2024.

September 2025 — DuckDuckGo Joins the AI Arms Race

- 4 September: DuckDuckGo upgrades its Duck.ai service with a paid subscription tier (£9.99/month). Subscribers gain access to GPT-4o, GPT-5, Claude Sonnet 4, and Meta Llama Maverick — all under DuckDuckGo’s no-tracking privacy terms. The free tier keeps GPT-4o mini, Claude 3.5 Haiku, and Llama 4 Scout.

- Agencies begin formally offering “Generative Engine Optimisation (GEO)” as a service line. The discipline is moving from niche to mainstream.

October 2025 — The Most Significant Regulatory Event in UK Search History

- 10 October: The CMA formally designates Google with Strategic Market Status (SMS) for general search and search advertising. The designation runs until 10 October 2030.

- The CMA confirms Google holds more than 90% of the UK search market. The designation covers Google Search, AI Overviews, AI Mode, Discover, and Top Stories.

- This is the most significant regulatory intervention in UK search since Google arrived in the market. The CMA can now impose mandatory conduct requirements.

- 22 October: The CMA separately designates both Apple and Google with SMS in mobile platforms.

November 2025 — ChatGPT Gets Smarter Again

- 12 November: OpenAI releases GPT-5.1, starting with paid subscribers. Two variants: GPT-5.1 Instant (warmer, better at following instructions) and GPT-5.1 Thinking (adaptive reasoning, faster on simple tasks). API access follows on 13 November.

- UK AI adoption continues to accelerate. Perplexity AI grows its UK user base significantly. Agencies without AI expertise begin losing pitches to competitors that have it.

December 2025 — The Year Closes with Maximum Volatility

- 11 December: Google launches the December 2025 Core Update — the third and final core update of the year.

- On the same day, OpenAI releases GPT-5.2, described as “the most capable model series yet for professional knowledge work.”

- The December update runs for 18 days, completing around 29 December. Volatility peaks on 13 December and again on 20 December. Content farms and thin-content sites are hit hardest.

- The year ends with UK search fundamentally different from how it began.

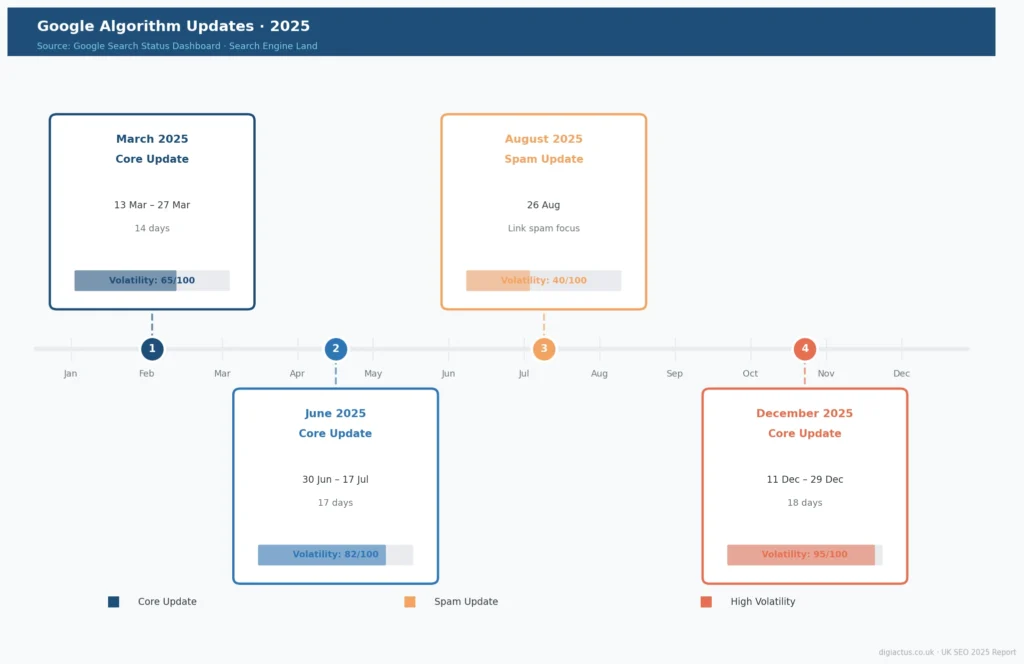

Google Algorithm Updates in 2025 — What Actually Changed

Google issued three core algorithm updates in 2025 (March, June, and December) and one spam update in August. The March update ran for 14 days, the June update for approximately 17 days, and the December update for 18 days. All three core updates emphasised E-E-A-T (Experience, Expertise, Authoritativeness, Trustworthiness) and helpful, people-first content. The August spam update targeted manipulative link schemes and low-quality backlinks.

The Four Updates at a Glance

| Update | Start Date | End Date | Duration | Key Focus |

|---|---|---|---|---|

| March 2025 Core | 13 Mar | 27 Mar | 14 days | Helpfulness, E-E-A-T; forum content recalibrated |

| June 2025 Core | 30 Jun | 17 Jul | ~17 days | YMYL sectors; partial HCU recoveries |

| August 2025 Spam | 26 Aug | Late Aug | Short | Manipulative links, backlink spam |

| December 2025 Core | 11 Dec | ~29 Dec | 18 days | Thin content; peaked volatility 13 & 20 Dec |

What the Updates Told Us About Google’s Direction

Several clear themes ran across all three core updates in 2025.

E-E-A-T became non-negotiable across all sectors. Previously, Google’s emphasis on Experience, Expertise, Authoritativeness, and Trustworthiness felt most relevant to health and finance (“YMYL”) sites. In 2025, it became a ranking factor for virtually every niche. Author credentials, editorial standards, and genuine first-hand knowledge all influenced rankings.

The Helpful Content System is now baked in. Google confirmed that its helpful content signals are no longer a separate layer — they are part of the core algorithm. This means there is no longer a separate “helpful content penalty” to recover from. Instead, helpfulness influences every ranking decision.

AI-generated content is judged on quality, not origin. Google’s own guidance (confirmed by John Mueller) states that the algorithm does not penalise content for being AI-generated. What it penalises is thin, low-quality, generic content — regardless of how it was made. Many sites that had relied on mass AI content without expert review suffered significant losses.

Forum content was corrected downward. Sites that had benefited from Google’s 2023 “hidden gems” update — which boosted forum and user-generated content — saw those gains partially reversed in the March 2025 update. Google appears to be rebalancing expert content versus crowd-sourced content.

Technical SEO still matters as a tiebreaker. Industry analysis suggests sites with a Largest Contentful Paint (LCP) above 3 seconds experienced around 23% greater traffic losses than faster competitors with comparable content quality.

UK Search Engine Market Share: Google, Bing, and DuckDuckGo

In 2025, Google held approximately 93% of UK search market share. Microsoft Bing held around 4%, and DuckDuckGo approximately 0.7%. Despite integrating GPT-5 into Bing via Microsoft Copilot, Bing did not gain material market share. The biggest shift was not between search engines — it was the growth of AI chatbots like ChatGPT as an alternative to search entirely.

How Market Share Actually Moved in 2025

| Search Engine | UK Share (mid-2025) | Trend vs 2024 | Notable Change |

|---|---|---|---|

| ~93.35% | Marginal decline from ~94.5% | AI Overviews on ~30% of queries | |

| Microsoft Bing | ~4.00% | Broadly flat | Copilot integration; no material share gain |

| DuckDuckGo | ~0.69% | Marginal uptick | Duck.ai subscription adds AI capability |

| Yahoo | ~1.0–1.5% | Declining | Legacy Bing partnership maintained |

| Others | <0.5% | Stable | No material UK movements |

Source: StatCounter UK data, 2025; Klatch analysis of StatCounter data.

The Bing Surprise: AI Integration Did Not Drive Market Share Growth

This is worth dwelling on, because it challenges a widely held assumption. Many analysts predicted that Microsoft’s deep integration of OpenAI technology into Bing — via Copilot — would drive meaningful share gains against Google. That did not happen.

StatCounter analysis shows that since ChatGPT launched publicly in November 2022, Bing’s UK share has actually drifted down by approximately 0.6 percentage points. The “Copilot effect” on market share was short-lived and negligible. Bing remained a distant second, largely used by default on Windows and Edge.

DuckDuckGo: Small but Purposeful

DuckDuckGo’s market share remained tiny at around 0.7%. However, its strategic direction is interesting. The Duck.ai subscription launched in September 2025 positions it as a privacy-first AI search alternative rather than a direct Google competitor. Its users are typically privacy-conscious, technically literate, and often willing to pay for a tracking-free experience.

The Real Competition: AI Chatbots, Not Search Engines

The most important competitive shift in 2025 was not between traditional search engines at all. It was the rise of ChatGPT, Perplexity, and Claude as genuine alternatives to Google for informational queries.

Ofcom data makes this clear: ChatGPT received 1.8 billion UK visits between January and August 2025 alone. Users are not switching from Google to Bing. They are switching from Google to AI chatbots for a growing range of queries — particularly research, comparison, and advice-type questions.

Zero-Click Searches: A Growing Problem

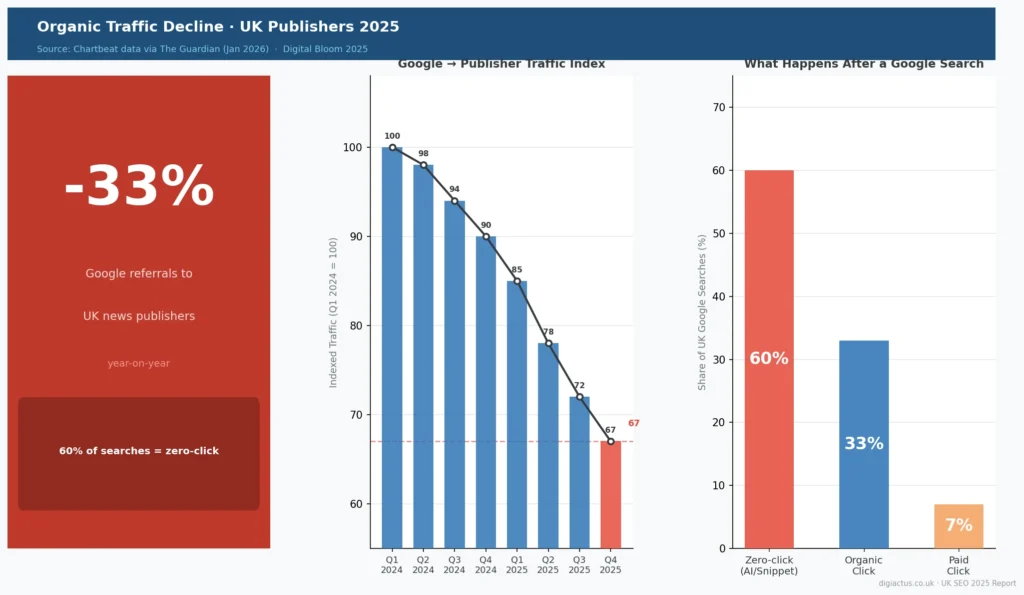

Even among users who still go to Google, the “click” is becoming less common. Around 60% of UK Google searches now result in no click to any external website (Digital Bloom, 2025). AI Overviews, featured snippets, and direct-answer features increasingly satisfy the query without the user ever visiting a site.

The AI Search Revolution: How ChatGPT and Gemini Changed Everything

By mid-2025, approximately 30% of UK Google searches triggered AI-generated summaries (AI Overviews). ChatGPT reached 252 million UK visits in August 2025, a 156% year-on-year increase. Google Gemini grew by 146% year-on-year, Anthropic Claude by 138%, and Perplexity by 100%. Ofcom described search as “moving away from conventional link-based pages toward AI-powered, chat-style interactions.”

The Ofcom Data — Verified

Ofcom’s Online Nation 2025 report, published December 2025, provides the most authoritative UK-specific data on this shift. All figures below are confirmed accurate against primary sources.

| AI Tool | Key UK Figure (2025) | Growth |

|---|---|---|

| ChatGPT | 252M UK visits in Aug alone; 1.8B Jan–Aug total | +156% YoY (vs Aug 2024) |

| Google Gemini | Strong UK adoption | +146% YoY (Jan–Aug) |

| Anthropic Claude | Strong UK adoption | +138% YoY (Jan–Aug) |

| Perplexity AI | Fastest-growing research AI | +100% YoY (Jan–Aug) |

| Google AI Overviews | ~30% of UK queries | Mainstream by mid-2025 |

Source: Ofcom Online Nation 2025, via Mobile World Live

The Major AI Tool Launches in 2025

Here is a clean summary of the key AI tools and updates that shaped UK search behaviour in 2025.

| Tool / Platform | Key 2025 Event | Date | UK Impact |

|---|---|---|---|

| ChatGPT (GPT-5) | GPT-5 launches across all tiers | 7 Aug 2025 | Became dominant AI search tool; 252M UK visits that month |

| ChatGPT (GPT-5.1) | Instant + Thinking modes released | 12 Nov 2025 | Smarter, more conversational answers |

| ChatGPT (GPT-5.2) | Most capable model for professional work | 11 Dec 2025 | Arrived same day as Google’s Dec core update |

| Google Gemini | Integrated across Search via AI Overviews | Throughout 2025 | Powers AI Overviews on ~30% of UK queries |

| Microsoft Copilot | GPT-5 integration from August | Aug–Dec 2025 | Slight enterprise uplift; no mass market shift |

| DuckDuckGo Duck.ai | GPT-5, Claude Sonnet 4 in paid tier | 4 Sep 2025 | Privacy-focused AI search option |

| Perplexity AI | Doubled UK user base | Jan–Aug 2025 | Research-oriented; growing among info-seekers |

What This Means for How People Search

The shift is not just quantitative — it is qualitative. Users are asking AI chatbots fundamentally different questions than they ask Google. Ofcom notes that the average ChatGPT prompt is around 23 words, compared to about 4 words for a traditional Google search. Users expect complete, synthesised answers — not a list of links to visit.

This has a direct impact on organic traffic. When users see an AI-generated answer, they are demonstrably less likely to click through to any website at all. Publishers and content sites have felt this the most. As The Guardian reported in January 2026 (citing Chartbeat data), Google referrals to news publishers fell by approximately 33% year-on-year — one of the starkest single-year declines on record.

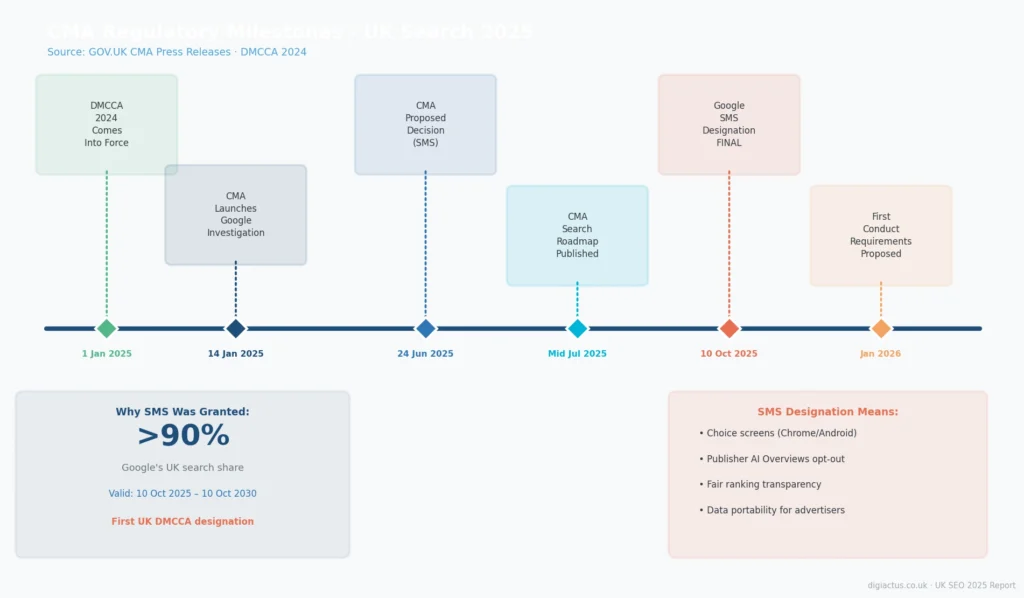

UK Regulation: The CMA’s Landmark Google Decision

On 10 October 2025, the UK Competition and Markets Authority (CMA) formally designated Google with “Strategic Market Status” (SMS) in general search and search advertising, under the Digital Markets Competition and Consumers Act 2024. This was the first SMS designation under the new law. It gives the CMA power to impose mandatory conduct requirements on Google — including user choice screens, fair ranking rules, data portability, and publisher controls over AI Overviews. The designation lasts until 10 October 2030.

The Timeline of Regulatory Action in 2025

| Date | Action |

|---|---|

| 1 Jan 2025 | DMCCA 2024 comes into force; CMA gains new Big Tech powers |

| 14 Jan 2025 | CMA formally launches investigation into Google’s search markets |

| 24 Jun 2025 | CMA publishes Proposed Decision provisionally designating Google with SMS |

| Mid-Jul 2025 | CMA publishes Search Roadmap: choice screens, data portability, publisher controls |

| 10 Oct 2025 | CMA Final Decision: Google formally designated with SMS (valid until Oct 2030) |

| 22 Oct 2025 | CMA also designates Apple and Google with SMS for mobile platforms |

| 26 Jan 2026 | CMA issues first Proposed Conduct Requirements for Google under SMS |

| 25 Feb 2026 | Consultation deadline for stakeholders on those requirements |

What Could Change for Businesses

The SMS designation is historic, but its practical impact depends on which conduct requirements the CMA actually imposes. Based on the Proposed Conduct Requirements published in January 2026, four areas are being prioritised:

1. User choice screens. Google may be required to give UK users on Chrome and Android the option to choose a different default search engine. This could shift a small but meaningful share of queries to Bing, DuckDuckGo, or others.

2. Fair ranking and transparency. Google may face requirements to be clearer about how algorithm changes affect businesses, and to provide faster resolution for businesses that experience sudden drops in visibility.

3. Publisher controls over AI Overviews. This is potentially the most significant for content creators. Publishers may be given the ability to opt out of having their content used to generate AI Overview summaries — without losing standard organic rankings as a result.

4. Data portability. Advertisers and analytics providers may get easier access to anonymised search data, enabling fairer competition.

The CMA has indicated final conduct requirements are likely to be imposed in the first half of 2026, with enforcement possible by the end of 2026.

How the Year Ended — and Where Things Stand Now

By December 2025, the search marketing industry looked very different from where it had started.

The year began with stable market shares, relatively familiar SEO practices, and a regulatory investigation that most businesses had not yet registered. It ended with:

- Three Google core updates completed, each reinforcing the same message: expertise and genuine helpfulness win

- GPT-5, GPT-5.1, and GPT-5.2 all live and in use by millions of UK users

- ChatGPT firmly established as a mainstream alternative for informational queries

- Google referrals to publishers down roughly 33% year-on-year

- The CMA’s Google designation formally changing the regulatory landscape

- Agency demand for SEO and PPC expertise at record levels

The narrative that best describes 2025 is this: traditional SEO was not made irrelevant, but the rules changed enough that those who had not adapted were clearly behind. The question heading into 2026 is not whether to adapt — it is how fast.

Sector-by-Sector Impact: Who Won and Who Struggled

In 2025 UK search, the biggest winners were SEO agencies (demand up 61–115%), large established brands, and subscription media. The biggest losers were news publishers (Google referrals down ~33%), content farms, generic blog networks, and businesses without any digital presence. E-commerce, finance, health, and local services saw mixed results — those with strong brand signals and structured data fared better than those relying on unbranded informational traffic.

Sector Impact Summary

| Sector | Verdict | What Drove It | Key Action |

|---|---|---|---|

| SEO Agencies & Freelancers | Strong growth | Demand +61–115% YoY; AI strategy services in high demand | Upskill in GEO; reposition as AI search strategists |

| News & Publishing | Significant decline | Google referrals -33% YoY; AI Overviews replacing article visits | Subscriptions, newsletters, original analysis |

| Large Brands & Retail | Resilient | Brand search remains strong; direct traffic holds up | Leverage brand equity; invest in first-party data |

| E-commerce (unbranded) | At risk | AI summaries answer comparison and product queries | Schema markup, AI shopping tools, strong brand identity |

| Finance & Insurance | Mixed | Regulated, authoritative content retains advantage | Double down on E-E-A-T; accredited authorship |

| Health (NHS, specialists) | Mixed | NHS/BMA retain authority; smaller health sites lose clicks | Medical schema, expert author signals |

| Local Services | Mixed | Local queries still mostly Google Maps/Assistant driven | Google Business Profile, local schema, reviews |

| Tech / SaaS / B2B | Variable | Generic content lost 70–80% traffic (e.g. HubSpot); proprietary tools grew | Be cited by LLMs; publish original data |

| SMBs with no digital strategy | Declining | Invisible to AI search; losing ground to stronger digital presences | Basic local SEO; Google Business Profile minimum |

The HubSpot Case Study — A Warning for Everyone

HubSpot became the most cited cautionary example in UK and global SEO discussions throughout 2025. The company, which had built enormous organic traffic through high-volume, generic “how-to” content, experienced a traffic decline of 70–80% after Google’s series of core updates revalued that type of content.

The lesson is not that content marketing is broken. It is that generic content written primarily for search volume — rather than genuine expertise — no longer holds its rankings when the algorithm has learned to recognise the difference.

Impact on Freelancers and Agencies

The Freelancer Picture

2025 was paradoxical for freelance SEO and content professionals. Demand surged, but the gap between those with AI skills and those without widened sharply.

Freelancers offering AI strategy, GEO consulting, prompt engineering, or technical SEO saw strong inbound enquiry throughout the year. The Koozai data (61–115% increases in agency searches) suggests that the demand explosion was real and sustained — not a short-term spike.

However, freelancers whose core offering was “keyword-optimised content writing” at volume found themselves undercut by AI tools and — more painfully — found that many of their clients had discovered the same tools. The value proposition of “I will write 20 blog posts a month for your website” became much harder to defend when AI could produce the same volume for a fraction of the cost.

The freelancers who thrived were those who could answer a different question: not “can you create content?” but “can you make sure this content actually earns visibility in AI search?”

The Agency Picture

For agencies, 2025 was broadly a growth year — but an uncomfortable one for those that had not invested in AI capability.

Agencies that rebranded or extended into GEO, AI content strategy, and AI search analytics picked up new clients and retained existing ones more easily. Those that continued offering purely traditional SEO packages found clients questioning the value more aggressively than in previous years.

The most successful UK marketing agencies in 2025 did several things differently. They trained their teams on AI tools. They built proprietary frameworks for measuring AI citation and visibility alongside traditional rankings. They offered clients clear explanations of how the changing search landscape affected their specific business — not just generic updates about algorithm changes.

One structural challenge emerged for smaller agencies: the cost of staying current. AI tools, analytics platforms, and training add up. Several smaller agencies found themselves in a difficult position — too small to absorb these costs easily, but too visible to clients to ignore the capability gap.

The Survival Imperative

The phrase that sums up the freelancer and agency situation in 2025 most accurately is this: the middle ground disappeared. Basic SEO commoditised rapidly. Sophisticated AI search strategy commanded premium rates. The space in between shrank significantly.

How to Adapt: A Practical Survival Guide

For SEO Agencies and Freelancers

Reframe your service offering. The discipline of “Generative Engine Optimisation (GEO)” is the natural extension of SEO into the AI era. Help clients be cited inside AI answers, not just ranked on page one of Google. These are increasingly different goals.

Master E-E-A-T as a deliverable. Audit your clients’ author profiles, credentials, and content depth. Build expert author pages. Create editorial standards documents. Demonstrate genuine expertise in every piece of content — not just topic coverage.

Make structured data a core deliverable. FAQ, HowTo, Product, LocalBusiness, and Organisation schema all improve the chances of content being surfaced in AI answers and voice results. This should be standard practice, not an optional add-on.

Diversify client traffic sources. Email newsletters, owned communities, and video content should be part of every client strategy. SEO alone — even excellent SEO — is no longer sufficient to protect organic revenue.

Track the new metrics. Traditional rank tracking is necessary but not enough. Monitor brand search volume, direct traffic, and AI referral sources. Platforms like Profound, SEMrush’s AI Visibility toolkit, and Writesonic now offer AI citation tracking across ChatGPT, Perplexity, Gemini, and Claude.

Position expertise as the product. Clients increasingly need someone who understands how their specific business is affected by the changing search landscape — not just someone who can write keyword-optimised content or build links.

For Brands and Businesses

Strengthen your brand signal. AI systems favour known, well-cited brands. Ensure your brand name appears consistently and in authoritative contexts across the web — not just on your own site.

Build first-party data infrastructure. Email lists, loyalty programmes, app users, and registered members are all assets that protect you from search traffic volatility. The businesses most resilient to the 2025 search changes were those that had audience relationships not dependent on Google.

Consider on-site AI tools. A GPT-powered chat assistant on your website captures queries that AI might otherwise answer off-site. Several UK retailers and financial services businesses launched these in 2025 to good effect.

Engage with the CMA process. If your business has been materially affected by AI Overviews — particularly if you are a publisher — monitor the CMA’s proposed conduct requirements. The publisher opt-out mechanism for AI Overviews could be a material lever for protecting content value.

Create content AI will cite. Original research, proprietary data, expert commentary, and clear definitions are the content types most likely to be cited by LLMs. Generic, derivative content has very little chance of appearing in AI-generated answers.

For Content Publishers

Invest in what AI cannot replicate. Original investigative journalism, exclusive data, expert commentary, and live reporting are the only content categories that consistently resist AI summarisation. The Financial Times, The Economist, and specialist trade publications showed that subscription models built on this kind of content can hold up even as search traffic declines.

Monitor the publisher opt-out mechanism. The CMA’s proposed conduct requirements include a mechanism for publishers to opt out of having their content used to generate Google AI Overviews — without penalty to their standard organic rankings. Watch this closely.

Rethink SEO metrics entirely. If your primary success metric is organic traffic volume, you will look like you are failing even when you are not. Engagement, time on site, newsletter sign-ups, return visits, and subscription conversions are more meaningful measures of health for publisher businesses in 2025 and beyond.

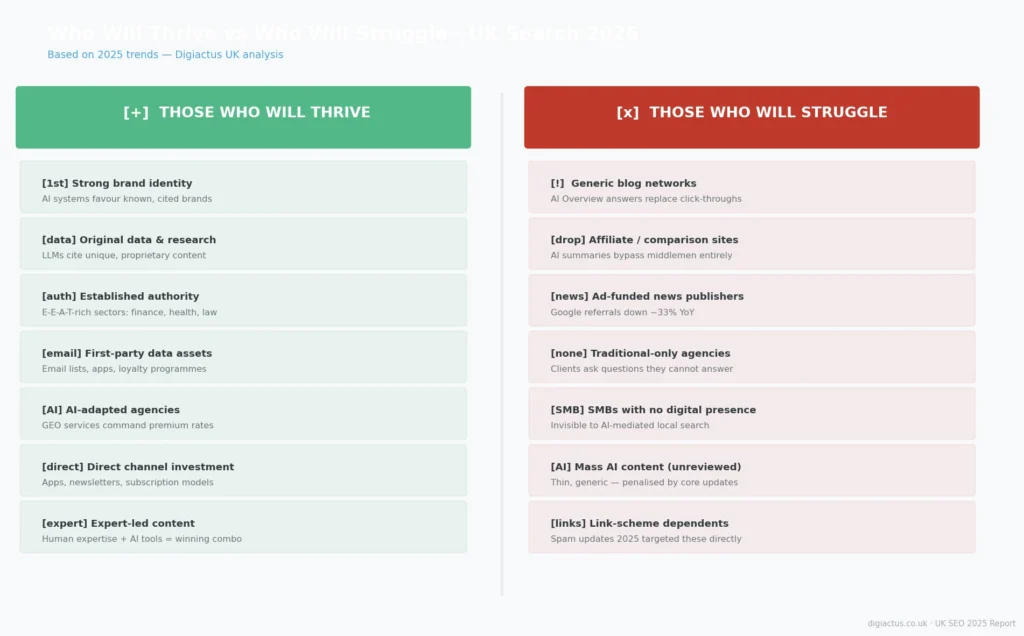

Who Will Thrive vs Who Will Struggle Going Forward

Those Ahead of the Curve

Some businesses and professionals will look back at 2025 as the year they pulled ahead. They will likely share most of these characteristics:

- They have strong brand recognition — their name is one people search for directly, and one AI systems reference when asked about their category

- They publish original, data-driven content that demonstrates genuine expertise

- They have first-party audience relationships (subscribers, registered users, loyal customers) that do not depend on Google for daily traffic

- They treated AI tools as a capability multiplier rather than a threat — using them to produce more and better work, not to replace quality with volume

- They adapted their service offering (for agencies) or their marketing strategy (for brands) early enough to build expertise before the demand surge priced out quick learning

Those Who Will Struggle

Some businesses and digital professionals face genuine risk. The warning signs are fairly consistent:

- Organic traffic accounts for 70% or more of their revenue, and that traffic is primarily informational rather than transactional

- Their content strategy is built around keyword volume rather than genuine expertise — producing answers that AI can now generate more cheaply

- They have not invested in understanding AI search, either as a tool to use or as a landscape to navigate

- Their brand presence is weak or non-existent on authoritative third-party platforms, meaning AI systems have no strong signal to cite them

- For local businesses: no Google Business Profile, no local reviews, no structured data — essentially invisible to the AI-mediated local search that is growing steadily

The dividing line in 2025 was not technology adoption for its own sake. It was whether businesses had genuine value to offer — and whether they had made that value legible to the systems (both human and AI) through which people now discover information.

Key Comparison Tables

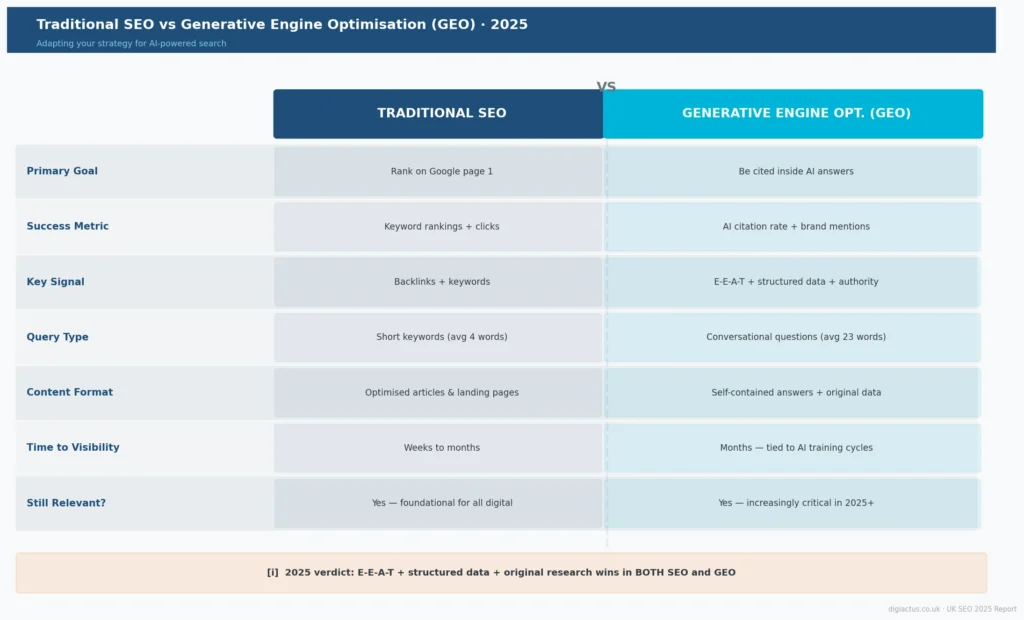

SEO vs GEO: Understanding the Difference

| Factor | Traditional SEO | Generative Engine Optimisation (GEO) |

|---|---|---|

| Primary goal | Rank on page 1 of Google | Be cited in AI-generated answers |

| Key ranking signal | Backlinks, keywords, technical quality | E-E-A-T, structured data, citation authority |

| Success metric | Keyword rankings, organic clicks | AI citation rate, brand mention frequency |

| Query type optimised for | Short keyword phrases (avg 4 words) | Conversational questions (avg 23 words) |

| Content format | Optimised articles and landing pages | Self-contained answers, direct definitions, original data |

| Time to visibility | Weeks to months | Months (AI model training cycles) |

| Still relevant? | Yes — foundational | Yes — and increasingly critical |

UK Search Engine Comparison 2025

| Feature | Bing (Copilot) | DuckDuckGo (Duck.ai) | Perplexity | |

|---|---|---|---|---|

| UK market share | ~93% | ~4% | ~0.7% | <0.5% |

| AI integration | AI Overviews (~30% of queries) | Copilot (GPT-5) | Duck.ai subscription (GPT-5, Claude Sonnet 4) | AI-native (all results) |

| Privacy | Standard data collection | Standard data collection | No tracking | Standard data collection |

| Best for | Everything | Windows/Enterprise defaults | Privacy-conscious users | Research queries |

| Regulatory status | SMS designated (CMA, Oct 2025) | Not designated | Not designated | Not designated |

2025 Google Core Updates Compared

| March 2025 | June 2025 | December 2025 | |

|---|---|---|---|

| Duration | 14 days | ~17 days | 18 days |

| Volatility | Moderate | Higher | Highest of the year |

| Most affected | Forum/UGC content | YMYL sectors | Thin content, content farms |

| Partial recoveries? | Some | Yes (HCU) | Some |

| E-E-A-T signal | Strong | Strong | Strong |

Impact by Business Type: Quick Reference

| Business Type | Short-Term Risk | Long-Term Risk | Priority Action |

|---|---|---|---|

| Large brand with strong direct traffic | Low | Low | Maintain brand signal; monitor AI citations |

| News publisher (ad-funded) | High | Very high | Subscription model; publisher opt-out (CMA) |

| SEO agency (AI-adapted) | Low | Low | Scale GEO services; build proprietary frameworks |

| SEO agency (traditional only) | High | Very high | Upskill immediately or face client attrition |

| E-commerce (branded) | Low–medium | Low | Schema, structured data, chat commerce |

| E-commerce (unbranded/affiliate) | High | High | Brand building, first-party data, AI strategy |

| Freelance content writer (AI-aware) | Low | Low | Position as AI-strategy expert, not just writer |

| Freelance content writer (volume-only) | High | Very high | Reposition toward strategy, editing, AEO |

| SMB with Google Business Profile | Low | Low | Maintain profile, local schema |

| SMB with no online presence | Very high | Extremely high | Start with basics: GBP, NAP consistency, FAQs |